Historically, the stock market declines about one year out of four. Another way of looking at this is that stock market increases have been positive, on average, three out of four years. This doesn’t mean that only one year (the down year) was volatile. Every year was volatile to the extent that the returns were all highly uncertain. Stocks can be highly unpredictable in the short term and extremely efficient in the long term.

Historically, the stock market declines about one year out of four. Another way of looking at this is that stock market increases have been positive, on average, three out of four years. This doesn’t mean that only one year (the down year) was volatile. Every year was volatile to the extent that the returns were all highly uncertain. Stocks can be highly unpredictable in the short term and extremely efficient in the long term.

It’s been said that investing is one part intellectual, nineteen parts temperamental. Often, the best chance for enhanced stock market returns is realized by holding them through a whole market cycle. This means having the temperament to embrace the ups and downs. Warren Buffett once said of Berkshire Hathaway, “We would make more money if volatility were higher because volatility would create more mistakes. Volatility is a huge plus to real investors.” Author and mentor Nick Murray says, “If you think the market’s ‘too high’ wait ‘til you see it 20 years from now.”

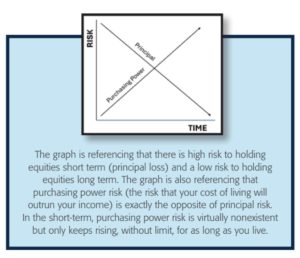

One of the biggest conflicts countless retirees face is the choice between growth and protection. You need to keep your income growing at the rate your cost of living is inflating. You also need protection so you won’t get wiped out by the next bear market. Do you forfeit growth for protection, or do you give up protection for growth?

In retirement, your financial life comes down to one simple question: Will your money outlive you, or will you outlive your money? A non-smoking 62-year-old couple has a joint life expectancy of about 30 more years. That means, on average, the second person will pass away around age 92. If you haven’t got a plan to grow your income AND protect your purchasing power, you may – by default – have a plan for running out of money.

Owners of good businesses make more money than their lenders. When you invest in stocks, you are the owner. When you invest in bonds, you are the lender. Wealth comes to the owner, not the loaner. This doesn’t mean you shouldn’t own bonds – bonds have their place in an investment portfolio, but building long-term wealth isn’t one of them.

The best solution is often a good plan. Sit down with a yellow pad and a No. 2 pencil to determine when your money will be needed. Set aside funds for emergencies and planned expenses. A sound strategy is to invest the portion needed for retirement income more conservatively to avoid extreme market fluctuations. The remaining balance can now be invested for long-term growth. The mortal enemy of volatility is time. Time in the market – as opposed to timing the market – is the key to capturing the superior returns of stocks.