Tax-efficient investing is the process of repositioning your investment portfolio into pre-tax, post-tax and tax-advantaged funnels. Tax-efficient investing looks at the tax makeup of your income and assets with the goal of getting you the most after-tax income for each dollar of savings. A typical investor has three funnels: Pre-Tax, Post-Tax and Tax-Advantaged.

Tax-efficient investing is the process of repositioning your investment portfolio into pre-tax, post-tax and tax-advantaged funnels. Tax-efficient investing looks at the tax makeup of your income and assets with the goal of getting you the most after-tax income for each dollar of savings. A typical investor has three funnels: Pre-Tax, Post-Tax and Tax-Advantaged.

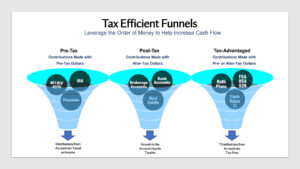

Pre-Tax Funnel (401(k)/IRA)

Most investors have a major portion of their retirement savings in tax-deferred investments. Generally, you will get a tax deduction for the contributions you put into this funnel, and you will pay taxes on your cumulative contributions and future earnings when you access your funds. You contribute $100,000 to your 401(k), it grows to $200,000, you take a $200,000 distribution and you are taxed on the $200,000 total.

Post-Tax Funnel (Bank/Brokerage)

This funnel is often used for savings above and beyond what can be contributed to tax-deferred or tax-advantaged accounts. You do not get a tax deduction for the contributions you put into this funnel, and you are required to pay taxes on your earnings each year. You contribute $100,000 to your post-tax brokerage account, it grows to $200,000, you take a $200,000 distribution and you are taxed on the $100,000 growth.

Tax-Advantaged Funnel (Roth/529 Plan)

Most investors have a smaller portion of their retirement savings in tax-advantaged investments. You do not get a tax deduction for the contributions you put into this funnel, and you won’t pay taxes on your cumulative contributions or future earnings when you access your funds. You contribute $100,000 to a tax-advantaged Roth IRA, it grows to $200,000, you take a $200,000 distribution and you pay zero tax.

There is a specific order for how you should save money during your accumulation years. Overfunding or underfunding a tax funnel could create unintended tax consequences during your retirement years.

Three questions to consider in retirement:

1. How much ordinary income should you take out of your pre-tax funnel?

2. How much income should you take out of your post-tax funnel that may be eligible for qualified dividend or long-term capital gain treatment?

3. How much additional income should you take out of your tax-advantaged funnel to blend out the maximum amount of income with the minimum amount of income tax?

IRA expert, Ed Slott, says “taxes will be the single biggest factor that separates people from their retirement dreams.” Unlike losses in the stock market, money lost to taxes never recovers. Since not all money is taxed the same, tax-efficient investing could be your path to greater wealth.